The Biggest Myth In the Market Just Broke

Listen to the audio version of this article (generated by AI).

In the spring of 1999, Wall Street reached a consensus. The dot-com rally, once the exclusive property of a handful of Silicon Valley darlings, was finally broadening out. Retailers were getting websites. Manufacturers were becoming “e-businesses.” Regional banks were upgrading their software.

But the irresistible ‘rising tide lifting all boats’ story was just noise before the signal reasserted itself.

Twenty-seven years later, the same consensus is back — different ticker symbols, same mistake…

Since ChatGPT’s debut in November 2022, the S&P 500 — the benchmark index of the 500 largest U.S. companies — has dramatically outperformed the S&P 500 Equal Weight Index.

The standard S&P weights its components by market capitalization, meaning the largest companies by value — the so-called ‘Magnificent 7’: Apple (AAPL), Nvidia (NVDA), Microsoft (MSFT), Meta (META), Amazon (AMZN), Alphabet (GOOGL), and Tesla (TSLA) — carry an outsized influence. The Equal Weight version, as the name suggests, gives every included company an identical 0.2% slice.

Same companies, radically different performance.

As you can see in the chart below, the S&P 500 is on a historic win streak of smashing the Equal Weight index.

The divergence between these two indices tells you, in a single picture, everything you need to know about where investor capital is really going…

The AI Market ‘Broadening’ Narrative Just Broke

For a brief moment in late 2025 and early January 2026, the equal weight index actually outperformed.

Small caps started catching bids. The rate-sensitive parts of the market showed signs of life. Cyclicals perked up. And predictably, the financial media erupted with bullishness.

“The rally is finally broadening!” they said. “Small caps are ready to break out!”

CNBC and Bloomberg filled slots with guests sounding supremely confident that the long overdue broadening of one of the most heavily concentrated stock market rallies in history was (finally) here.

They were wrong. The Iran War saw to that.

The fresh geopolitical turmoil led to $90-plus oil, 3%-plus inflation, and a 10-Year Treasury yield above 4.3%. That formed a toxic cocktail for rate-sensitive, margin-thin businesses.

Small caps — which disproportionately carry floating-rate debt — took a hit. Consumer-facing businesses got squeezed from both ends. Healthcare stocks struggled because of higher rates. Financials did, too.

Meanwhile, since the war started, AI stocks have soared to new highs.

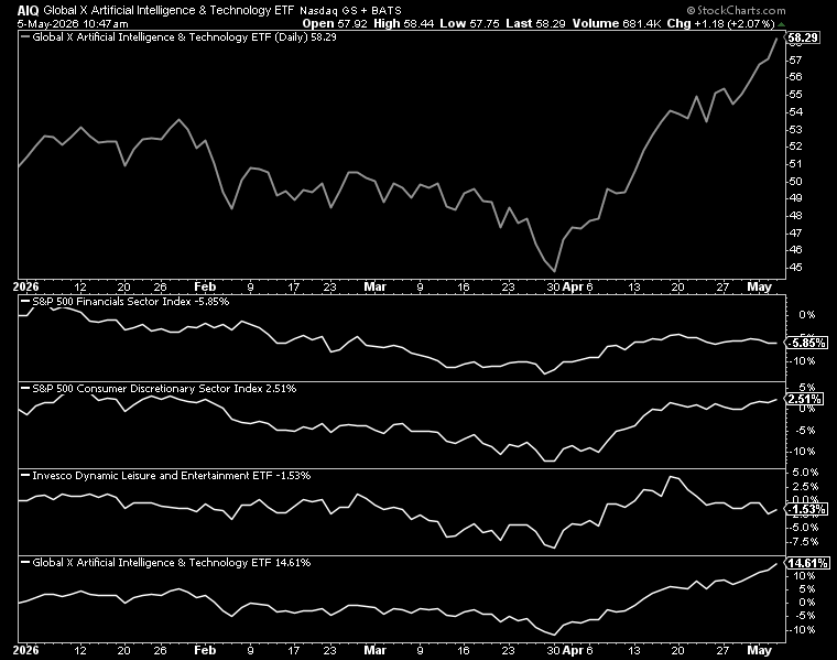

Take a look at the following chart, which shows the change in AI stocks — represented by the Global X Artificial Intelligence & Technology ETF (AIQ) — compared to the S&P’s financials and consumer discretionary sectors, as well as the Invesco Leisure and Entertainment ETF (PEJ).

While the rest of the market strains for gains, AI stocks just keep on winning.

And now the S&P 500 is back to smashing the Equal Weight Index, with the SPW/SPX ratio essentially back to 20-year lows.

So much for the “broadening out” thesis…

What AI Market Concentration Actually Looks Like

Instead, the market is just consolidating around the most powerful growth theme in a generation.

OpenAI recently raised $120 billion — not as a lifeline, but as a war chest.

Claude’s creator, Anthropic — one of the top-tier AI safety and research labs — just received $65 billion in commitments from two of the most capital-disciplined technology companies in the world. Amazon has agreed to pour up to $25 billion into the company. Google followed with a $40 billion pledge of its own. These are strategic bets by companies that know the AI arms race is winner-take-most.

Intel (INTC) — a company that spent most of the past decade as the semiconductor industry’s cautionary tale — just reported its best numbers in years. In fact, the chip sector, broadly, is on a record-long winning streak.

And then there is orbital compute — the emerging thesis that the next frontier of compute infrastructure will be built in space. Venture capital, defense contracts, and hyperscaler R&D are converging on a single conclusion: the Earth is running out of room for the AI buildout, so we are going off-planet. Elon Musk is talking about launching data centers into space. Google has a project with Planet Labs (PL) to do just that in 2027. And Meta has signed a deal with startup Overview Energy to beam space-based solar energy to Earth so it can power its terrestrial data centers.

We’ve moved beyond science fiction or speculative narrative here. The capital is real, the contracts are signed, and the infrastructure is being designed now.

The Real Risks to AI Stocks Aren’t Internal

Of course, this is where most AI bulls get sloppy. They stop asking “what could go wrong?” But discipline means actively monitoring for warning signs.

Right now, earnings from across the AI sector have been strong. Capital commitments are accelerating. New verticals like orbital compute are expanding the total addressable market rather than crowding it.

The fundamental momentum is, by any reasonable measure, exceptional.

Therefore, the risks worth watching are not internal to the AI sector. They are exogenous: a major credit event, a geopolitical escalation beyond Iran, a policy shock targeting semiconductors specifically.

The sector’s own fundamentals are essentially self-reinforcing. Hyperscaler capex funds chip demand. Chip demand drives infrastructure buildout. Infrastructure buildout enables new AI capabilities. New capabilities unlock new capital raises. And so the cycle continues.

The AI complex is not going to warn you when the trade gets crowded. The macro might — so keep your antennae up for what is happening outside the sector.

The Bottom Line: The AI Trade Is Deepening

The broadening thesis had a brief moment in the sun. Then the data turned against it; and the Iran War accelerated the reversal.

Now we are back to the reality that this bull market has one engine: AI.

The smart money is not diversifying away from AI right now. It is concentrating within it. And the data — both the technical picture in the SPW/SPX ratio and the fundamental picture in earnings, capital raises, and new market verticals — is corroborating that posture.

Own the AI infrastructure stack, the semiconductor supply chain, and the hyperscalers funding the buildout. Resist the siren song of talking heads telling you the next great opportunity is in small caps or consumer cyclicals or whatever other thesis works for a few fleeting moments.

The AI trade isn’t broadening — it’s deepening.

So don’t look wider.

Look downstream.

Because when capital floods into one system like this, it doesn’t just sit in chips or servers. It starts moving — through payments, platforms… whatever sits between users and their money.

That’s where we see the next great leverage forming.

And it’s why our attention has shifted to what Elon Musk is building with X.

See why.