The AI Capex Bear Case Just Lost Its Best Argument

Exponential View’s data just closed the door on the most compelling bear thesis in the market

Listen to the audio version of this article (generated by AI).

When the first American railroads began reporting revenue in the 1840s, the critics who had called the whole enterprise an overbuilt fantasy found themselves with less and less to say.

Something similar is happening in AI right now.

Exponential View just published the most comprehensive accounting of the AI economy we’ve yet seen — its State of the AI Economy 2026 report — with real revenue, utilization, and capex payback math.

The numbers don’t leave much room for the bear narrative.

The Revenue Bears Have Run Out of Excuses — $175 Billion Says So

Exponential View’s report estimates the global ex-China Generative AI (GenAI) economy is producing $175 billion in annualized revenue. And before anyone accuses Exponential View of creative accounting — this figure excludes chips, AI ad uplift, legacy software “AI features,” and financing.

In other words, it is only reflecting real customer demand.

Now, $175 billion in run-rate revenue sounds massive — and it is. But let’s contextualize that number.

One hundred seventy-five billion dollars represents just 0.5% of total U.S. GDP. The broader ‘digital economy’ sector makes up about 10% of GDP. Total U.S. corporate profits — which surged to a record $4.426 trillion in Q1 of 2026 — are 25x larger than the entire GenAI revenue pool. AI revenue is enormous in absolute terms and almost minuscule in relative terms.

Therein lies the opportunity…

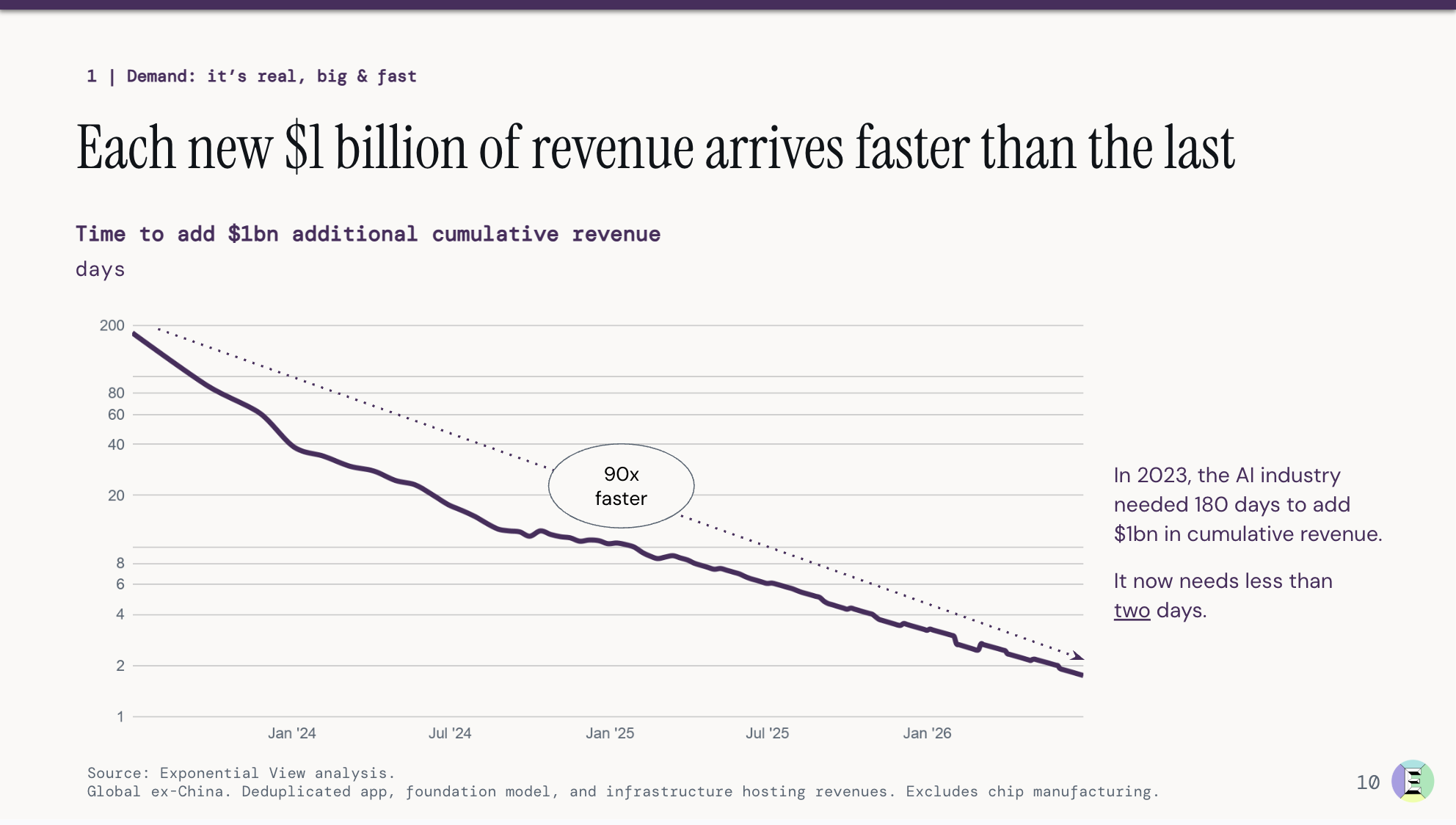

Because here’s the thing those relative numbers don’t capture: speed. AI revenue relative to GDP is already up 10x from Q1 2024. GenAI is scaling 3x faster than prior IT waves — faster than the internet and mobile booms. In 2023, the AI economy needed 180 days to add $1 billion of cumulative revenue. Today it needs less than two days. That is a 90x acceleration in the speed of revenue generation. Recent quarter-over-quarter growth is running ~35%, which annualizes to more than 3x.

This is the setup every long-term investor dreams about. Big enough to validate the thesis. Small enough that the runway is virtually unlimited. The penetration curve is in the very earliest innings of a generational platform shift — and the data proves it.

The CapEx Math Is Actually Working

According to the bears, while the hyperscalers are spending a combined ~$2 trillion cumulatively through 2026 on AI infrastructure — the largest technology buildout in history — there’s no possible way the economics ever pencil out. It’s a capex bubble about to burst.

Except… the math is starting to work.

The AI economy is now generating enough revenue to cover depreciation: the ongoing cost of using up the infrastructure built to run it. Not with room to spare, but the gap has closed, and the direction is positive.

For every dollar of AI infrastructure that depreciates, roughly $1.19 in hyperscaler and neocloud revenue is coming in to cover it — and $1.32 when you count the full GenAI economy. A year ago, that ratio was below 1. Now it’s above it.

This is still a race, of course. But the critics who insisted AI would never generate sufficient revenue to justify the buildout are already being proven wrong. And we are still in the early stages of the utilization ramp.

The Jevons Paradox: Why Falling Token Prices Are Bullish for AI

One of the more sophisticated bear arguments has to do with token cost. Some believe that as token prices continue to collapse — with blended pricing falling from ~$17 per million tokens to ~$2 —AI companies are destroying the economics of the industry.

‘Margins are going to zero. The boom is over.’

But that argument confuses price with value — and ignores how technology adoption actually works.

For technologies with elastic demand, falling prices create value; cheaper tokens = more use cases.

Better models expand what AI can actually do. Reasoning models consume more tokens as they think through complex problems. So the very thing bears are pointing to as a headwind — price compression — is actually the accelerant for the next leg of volume growth.

More apps, more agents, more inference, more memory, more networking, more storage, more power, more cooling, more data centers…

The Jevons paradox — the observation that efficiency improvements in resource use lead to increased total consumption — is playing out in real time across the AI infrastructure stack.

Bears are worried about price compression. Bulls are focused on volume elasticity. The data says volume wins.

Why AI Feels Slower Than It Is — and Why That’s Exactly What the Data Predicts

Here is one nuance worth understanding, because it explains why AI’s impact can feel underwhelming in GDP statistics even as it is very real inside companies.

Seven in 10 GenAI claims from companies in the S&P 500 focus on cost savings, time savings, throughput, or quality improvement. Explicit revenue gains are only ~6% of claims. The first killer enterprise AI app is not “create a magical new business line.” It’s “do the same work faster, cheaper, better.”

This is actually the normal pattern for platform shifts. The efficiency wave always comes first. Productivity gains show up in margins and labor leverage before they show up in GDP or revenue. The internet’s first decade was dominated by cost reduction and efficiency. Revenue came later — and when it came, it was enormous.

AI is following the same script. Efficiency now. Revenue later. And if the efficiency wave alone is already generating $175 billion in run-rate demand, imagine what happens when the revenue wave hits.

What the Revenue Inflection Means for AI Infrastructure Stocks Right Now

The macro data on AI has never been more bullish. The micro data — real company revenues, utilization trends, and capex payback — is inflecting positively. And yet AI stocks have been choppy, volatile, and in some cases well off their highs.

That combination — improving fundamentals, weak stock prices — is the definition of a buying opportunity.

The names best positioned to benefit from this data are across the full AI Builder stack, detailed most recently here:

- Chips and semiconductors

- Memory

- Networking and optics

- Servers and infrastructure

- Power and cooling

The Bottom Line: The Direction Changed

For the past two years, the race between AI capex and AI revenue has been the central question of this trade. This quarter, for the first time, the revenue side pulled ahead.

That doesn’t mean the race is over. The capex curve will keep rising. But the direction has changed — and in markets, direction matters more than destination.

The AI trade is alive, the fundamentals are inflecting, and the market is handing you a discount on one of the most compelling long-term growth stories in history.

That doesn’t happen often. Act accordingly.

Here’s one way to do that.

The infrastructure data in this piece tells you the AI buildout is real and accelerating. What it doesn’t tell you is where the most sophisticated private capital has already been positioning — months before this quarter’s numbers made the bull case undeniable.

Peter Thiel’s answer? A wholesale exit from public markets and a move into the physical substrate of the AI economy — the hard assets that get paid regardless of which model, which hyperscaler, or which application layer ultimately wins.

Most of those positions aren’t available to retail investors. Seven of them have a publicly traded equivalent.

Here’s what that portfolio looks like — and the thesis behind every position.