AI Broke the Digital Economy – And Almost Nobody Has Noticed

The next wave of AI winners won’t look like the last, and the rotation is already underway

AI didn’t supercharge the digital economy. It broke it.

For 40 years, America built an economy around software and services. We shipped factories overseas, hollowed out industrial capacity, and told two generations that prosperity lived behind a screen, not on a shop floor.

It worked spectacularly.

Technology became the foundation of American wealth – Apple (AAPL), Microsoft (MSFT), Alphabet (GOOGL), Amazon (AMZN), Meta (META). By 2025, tech and tech-adjacent companies made up more than 30% of the S&P 500, with just a handful of names driving a massive share of total market returns.

Then AI arrived.

And instead of making software more valuable… it started making it cheaper.

That’s the part most investors still haven’t fully processed.

Because the entire digital economy was built on one assumption: intelligence is scarce.

It took teams of highly paid engineers years to build products that could process payments, optimize logistics, serve ads, or manage enterprise workflows. That scarcity created moats. And those moats created trillions in market value.

AI is systematically removing that scarcity.

When intelligence can be generated on demand – faster, cheaper, and at near-zero marginal cost – the economics of software begin to change. Not all at once, and not for every company, but directionally and persistently.

And when that happens, value moves.

That shift has a name.

We call it the Great Re-Materialization – a reversal in where value accrues in the economy, from digital services back to physical infrastructure, energy, and raw materials.

Most investors are still positioned for the old world.

The market is already starting to price the new one.

The Shift From Software to Physical Infrastructure

The Re-Materialization is a fundamental inversion of where value accrues in the economy – from digital services back to physical infrastructure, raw materials, and hard assets.

To understand why it’s happening, you need to understand the original premise of the digital economy.

Software was valuable because intelligence was scarce. It took brilliant engineers years to build the systems that could stream movies, process payments, optimize logistics, serve relevant ads, and manage enterprise workflows.

That scarcity created defensible moats. And those moats created trillions of dollars in market value.

AI has systematically attacked that scarcity.

This Is Where the Moat Starts to Break

When a sufficiently capable AI can replicate the core function of most software applications – for approximately the cost of electricity – the moat begins to drain. Not all at once, and not for every company, but the directional pressure is unmistakable.

Enterprise Software-as-a-Service (SaaS) faces AI-native competitors built by 10-person teams. Consumer apps built on recommendation algorithms are vulnerable to AI agents that simply do the task rather than help you navigate an app. The advertising stack – Google and Meta’s financial foundation – faces meaningful disruption as AI agents begin browsing and buying on behalf of humans.

In the AI economy, the bottleneck isn’t intelligence. It’s compute. And compute is physical.

The cloud may be intangible, but the GPUs that operate it are not. They live in data centers – massive physical constructs that consume billions in steel, copper, concrete, and specialized equipment. Those data centers need extraordinary amounts of power, enough to strain a grid that was never designed for this kind of demand. That power needs to be generated, transmitted, and managed by physical infrastructure that takes years to build. In fact, data center electricity demand in the U.S. is projected to more than double by 2030, according to multiple industry estimates.And the GPUs themselves generate enormous heat, requiring sophisticated cooling systems made of copper tubing, heat exchangers, and specialized fluids.

This entire ecosystem needs to be connected by fiber optic cable, networking equipment, and physical connectivity infrastructure. And underpinning all of it: copper, silver, aluminum, rare earth elements, natural gas, water.

The physical cascade from GPU to raw material – this is where value accrues in the AI economy, not in the software sitting on top of it.

The market is just beginning to figure this out.

Why AI Infrastructure Stocks Are Leading the Market

Year-to-date in 2026, some of the strongest performers in the market read like an industrialist’s shopping list:

- Vertiv (VRT) – data center power and cooling – ~+67%

- Modine Manufacturing (MOD) – thermal management – ~+50%

- TTM Technologies (TTMI) – circuit boards – ~+41%

- Corning (GLW) – fiber optic cable – ~+53%

- Comfort Systems (FIX) – industrial HVAC and construction – ~+55%

- Texas Pacific Land (TPL) – physical acreage – ~+87%

- Bloom Energy (BE) – distributed power generation – ~+83%

All physical companies; “boring,” in many cases.

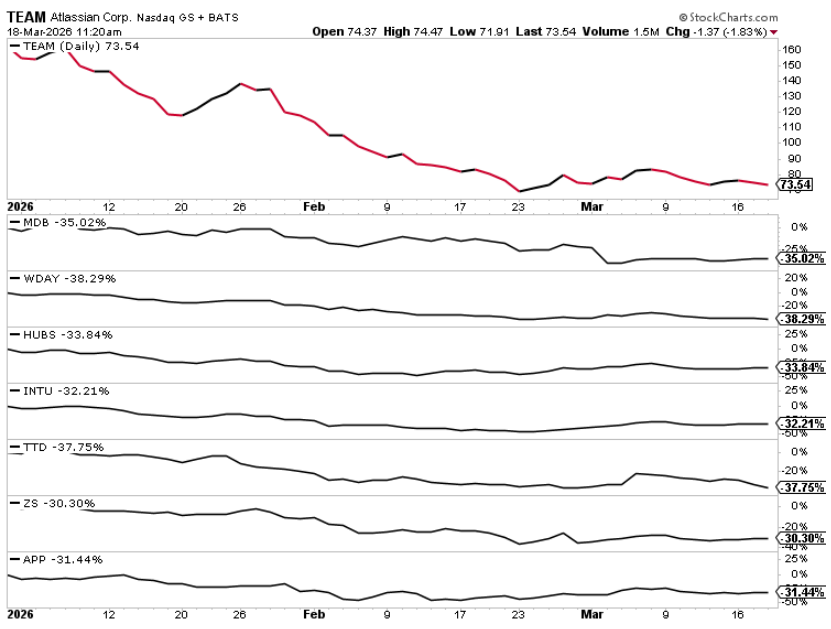

Meanwhile, some of the weakest performers were investor darlings just a few years ago: Atlassian (TEAM), MongoDB (MDB), Workday (WDAY), HubSpot (HUBS), Intuit (INTU), The Trade Desk (TTD), Zscaler (ZS), AppLovin (APP). Every one is a software play.

The market is already sending a signal. The question is whether you’re reading the returns or explaining them away.

Three Forces Behind the Shift to Physical Assets

Three forces are accelerating this shift simultaneously, and they’re not going away:

First, the compute arms race has no ceiling in sight. The hyperscalers – Microsoft, Google, Amazon, Meta – collectively are on track to spend over $600 billion on AI infrastructure in 2026. That number continues to rise. Every dollar of that capital flows into the physical stack: chips, facilities, power, cooling, connectivity, construction. The software sitting on top gets commoditized. The physical infrastructure that runs it becomes more valuable.

Second, America is trying to re-industrialize in a hurry. Between the CHIPS Act, the Infrastructure Investment and Jobs Act, and a wave of tariff policy designed to push manufacturing back to domestic shores, there is a coordinated policy push – from both parties, for different reasons – to rebuild the physical economy we spent 40 years dismantling. The reshoring trend is real and gaining momentum. It is inflationary for physical assets and deflationary for the digital services that were supposed to replace them.

Third, the energy grid is under growing strain – and AI is a major reason why. U.S. power demand had been essentially flat for 20 years before AI data centers arrived. Now utilities are scrambling. Grid infrastructure – transformers, switchgear, substations – has years-long backlogs. Natural gas peaker plants are being recommissioned. Nuclear restarts are being fast-tracked. Many critical components of the power stack are now in short supply. This is not a short-term problem. This is a decade-long capital cycle, and it’s just getting started.

Why the AI Infrastructure Boom Is Still Early

The investors who have noticed the Re-Materialization trade so far have mostly been playing the obvious first layer: Nvidia (already priced for perfection), the hyperscalers themselves (priced for dominance), and a handful of data center real estate investment trusts (REITs).

The second and third-order effects – the physical infrastructure, the raw materials, the energy buildout, the industrial supply chain behind all of it – remain underpriced relative to the scale of capital likely to flow through them.

Consider the scale of what’s coming. McKinsey estimates AI could add $13 trillion to the global economy over the next decade. Goldman Sachs sees $7 trillion. Even the bears see a multi-trillion-dollar wave. The overwhelming majority of the capital required to enable that wave has to be spent on physical things before a single dollar of software revenue can be generated.

You have to build the data center before you can run the model, mine the copper before you can wire the facility, install the transformer before you can power the GPU.

Meanwhile, the supply side of the physical economy is structurally constrained. We didn’t just outsource manufacturing. We also stopped training electricians, building transformer factories, and investing in copper mines. The lead time to bring new copper production online is eight to 12 years. Bringing a new domestic transformer factory online is another years-long endeavor. And the skilled trades workforce that would build all of this has been aging out for two decades, with no pipeline to replace it.

What you get when you combine surging AI-driven demand with structurally constrained supply is a sustained, multi-year commodity and infrastructure super-cycle. We are in the very early innings of that cycle.

The investors who made fortunes in the original AI trade bought Nvidia when it was a gaming graphics company that happened to make chips useful for training neural networks. The investors who make fortunes in the Re-Materialization trade will have bought copper miners, power equipment manufacturers, and industrial constructors before the mainstream financial media figured out that AI runs on copper.

The Winners of the AI Infrastructure Trade

The Re-Materialization has a winners list and a losers list. They are reasonably intuitive once you accept the thesis. Acting on them, however, requires fighting some deeply ingrained habits.

The winners are HALO stocks: Hard Assets, Low Obsolescence. These are companies whose value is anchored in physical assets that cannot be commoditized by software and whose core business is accelerated – not threatened – by AI demand. Power equipment manufacturers don’t get replaced by GPT-6. Copper miners benefit from every new data center that gets built. A thermal management company prospers every time a new GPU cluster comes online.

We see five HALO categories worth owning:

Data Center & Infrastructure Stocks

Power equipment, cooling systems, optical networking, data center construction specialists, printed circuit board manufacturers – these are the physical picks-and-shovels plays for the AI buildout.

Vertiv, Modine, Corning, Comfort Systems, TTM Technologies are representative names.

Energy and Power Generation

The grid cannot support AI demand in its current form. Natural gas, nuclear, and distributed generation are all beneficiaries.

Generac (GNRC), Bloom Energy, and any credible nuclear restart play deserve a place in the conversation.

AI Metals and Materials

Copper is the oil of the AI economy – you cannot build any of this without it. Silver has critical industrial uses in electronics and conductors. Aluminum, platinum group metals, and rare earths round out the materials complex.

Miners and royalty companies in these categories look cheap relative to the demand cycle ahead.

Industrial Logistics and Transport

An economy that needs to build things again needs to move materials and equipment at scale. Physical logistics operators benefit from re-shoring and the AI buildout construction wave.

Real Assets and Strategic Land

Royalty interests, water rights, land holdings in areas of energy or mineral significance… Texas Pacific Land is the canonical example – a company sitting on physical acreage that quietly became strategic real estate for the energy transition.

The losers in the Re-Materialization are the software stack. Not all of them, of course – those who own the physical compute infrastructure (i.e. Nvidia, the hyperscalers) will be fine, and the truly AI-native platform winners will emerge.

But the sprawling universe of enterprise SaaS, digital advertising middlemen, consumer apps, and cloud-native services built on the premise that software intelligence commands a permanent premium? That universe is facing a sustained repricing as AI commoditizes its core value proposition.

If your portfolio is heavy on companies that charge subscription fees for workflow software that an AI agent can now do for less, it’s time to take a hard look at those positions.

The Workforce Mismatch In the AI Economy

The investment implications are significant. The societal ones are even bigger.

The United States told generations that the path to economic security ran through knowledge work. Learn to code. Get a STEM degree. Develop skills in software, finance, law, data science. These jobs are the future; trades are the past. Millions of Millennials and Gen Zers built their lives, took on student debt, and made career decisions based on this promise.

AI is gradually putting that promise under pressure. It’s not happening all at once or for every role, but the pressure is undeniable, and the direction is clear. Meanwhile, the physical economy – the one we told people to leave behind – is desperately short of workers. There are not enough electricians to wire the data centers, not enough technicians to install the cooling systems, not enough grid engineers to build the transmission infrastructure. The skills America needs to win the AI economy are the exact skills it spent decades discouraging people from developing.

That is a political and social pressure point waiting to surface.

The labor shock from the Re-Materialization hasn’t fully hit yet – but it’s coming. When it arrives, the political response will be significant, and investors should be thinking about what that looks like. Infrastructure stimulus. Trade protection. Workforce retraining programs. All of it is inflationary for physical assets and physical businesses.

There’s also the market concentration problem. The S&P 500 is not a diversified index of the American economy. It is, at this moment, heavily concentrated in software and digital services. The top 10 holdings – nearly all tech and platform companies – represent over a third of the entire index.

If the Re-Materialization thesis plays out as we expect, the companies that need to reprice are the ones that will drag the broad market with them. That means the rotation out of software and into physical assets has implications for anyone with a passive 401(k) allocation – which is to say, most American investors.

The Bottom Line: AI Is Driving a Shift to Physical Assets

The great irony of the AI revolution is this: the technology that was supposed to be the apex expression of the digital economy turns out to be its most powerful disruptive force.

AI is not making software more valuable. It is making running software more valuable – and running software requires an enormous, expensive, and increasingly scarce physical substrate.

America spent decades building the wrong economy for this moment. We have too much software and not enough infrastructure, too many coders and not enough electricians, too many SaaS subscriptions and not enough copper mines.

The Re-Materialization is the market’s slow, inexorable process of correcting that imbalance.

The trade is already underway. The physical stack is outperforming, while the software stack is struggling. And we are, by any reasonable assessment, still in the first act.

The investors who recognize what’s happening – who understand that the hidden architecture of the AI economy runs on GPUs, data centers, copper wire, cooling fluid, and kilowatts rather than clever algorithms – have a generational opportunity in front of them.

Those who keep buying the consensus digital economy portfolio because “the big tech companies will figure it out” may be in for a very different few years than they expect.

The first wave of the AI boom rewarded the obvious winners.

The next wave will reward the companies positioned closest to where value actually concentrates.

And right now, there may be no company more central to that question than OpenAI.

Not because of what it is today… but because of what it could become once it steps into public markets.

I’ve broken down how that transition could unfold – and what it may mean for investors paying attention early.

You can explore it here.